6800 SW 40th Street #159

Miami, FL 33155-3708, USA

contact@6040forveterans.com

The 60/40 Business Method is a structured housing stabilization framework designed to address affordability challenges through a legally defined and adaptable approach. Rather than relying on a single rigid obligation, the method applies a segmented mortgage concept that balances immediate payment sustainability with long-term financial stability.

This methodology is built to operate within existing legal, financial, and policy environments, allowing for compatibility with current mortgage regulations, tax frameworks, and public-interest housing objectives. Its design emphasizes transparency, enforceability, and clearly defined obligations over the life of the mortgage.

By aligning payment responsibility with real-world economic capacity, the method seeks to reduce systemic payment stress while preserving ownership continuity and long-term asset integrity. The approach is intended to function as a practical, repeatable framework that can be evaluated, regulated, and implemented at scale under appropriate authorization.

Establishes a long-term structure intended to support equity recovery over the life of the mortgage under stable participation and market conditions.

Designed to operate within existing legal and tax frameworks and to remain compatible with established public-policy tools where applicable.

Focuses on sustainability of the adjusted monthly obligation, supporting evaluation based on realistic payment capacity rather than rigid legacy thresholds alone.

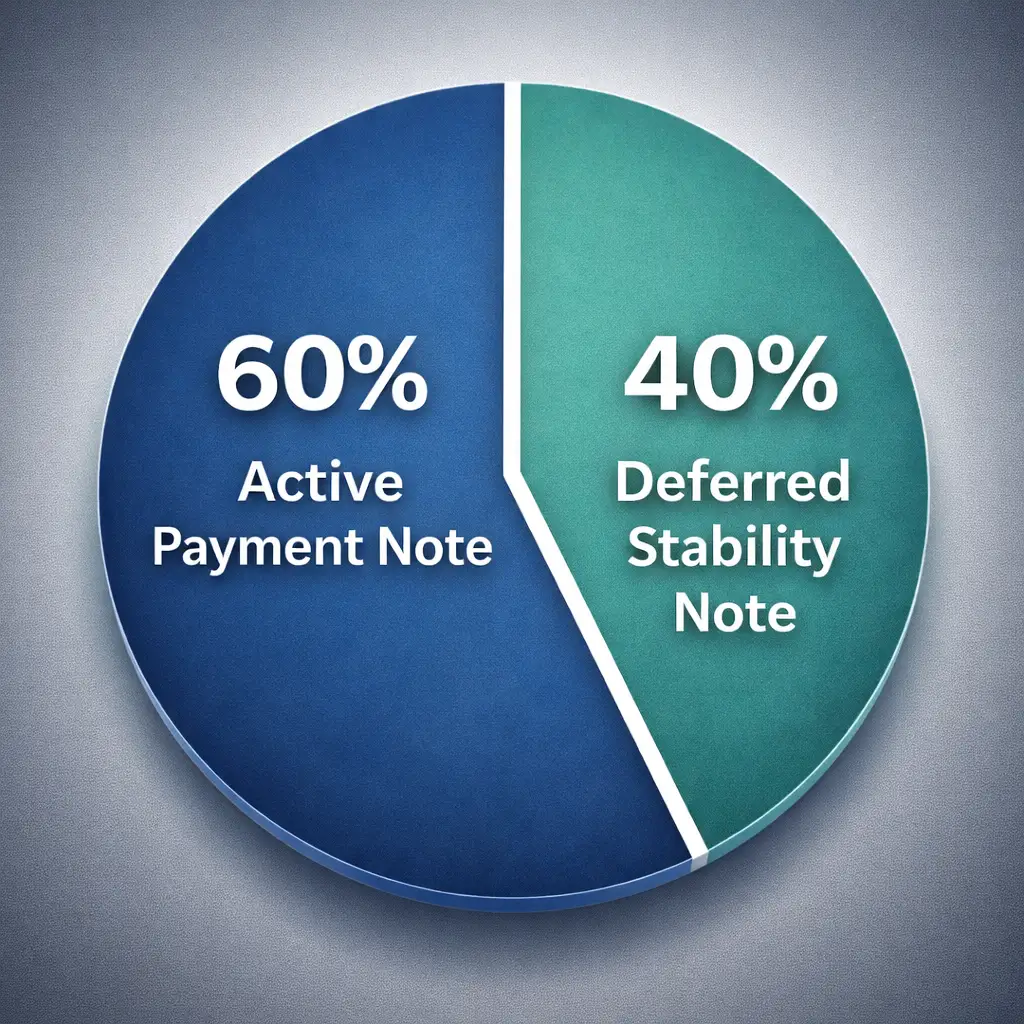

One Mortgage — Two Notes (60/40)

Both notes are legally recorded and secured under a single mortgage.

One mortgage secures two separate promissory notes, each recorded and enforceable under program rules.

Note A represents 60% of the mortgage balance and is paid through 360 equal, consecutive, zero-interest monthly payments following a 60-day post-closing stabilization period.

Note B represents the remaining 40% of the balance, carries zero interest, requires no monthly payments, and remains outstanding until a qualifying title-related event occurs.

NAt any title-related event outside program rules—including sale, refinance, or transfer—both Note A and Note B must be fully satisfied or properly assumed by an eligible participant.

Active Payment Note

Both notes are legally recorded and secured under a single mortgage.

Deferred Stability Note

Both notes are legally recorded and secured under a single mortgage.

(FINAL RULES)

Total closing costs equal 4.15% of the total mortgage amount (Note A + Note B) and are assessed at closing.

For participants experiencing financial hardship:

(DTI/DTR)

Affordability is evaluated using conservative standards such as:

For veterans on fixed income, disability, or severe affordability stress:

Taxes and insurance may be included only if the total monthly housing obligation remains within the applicable affordability cap .